Have you ever watched a high-stakes poker game where someone suddenly drops a massive stack of chips right in the middle of the table, completely changing the energy of the room?

That is exactly what just happened in the Indian banking landscape.

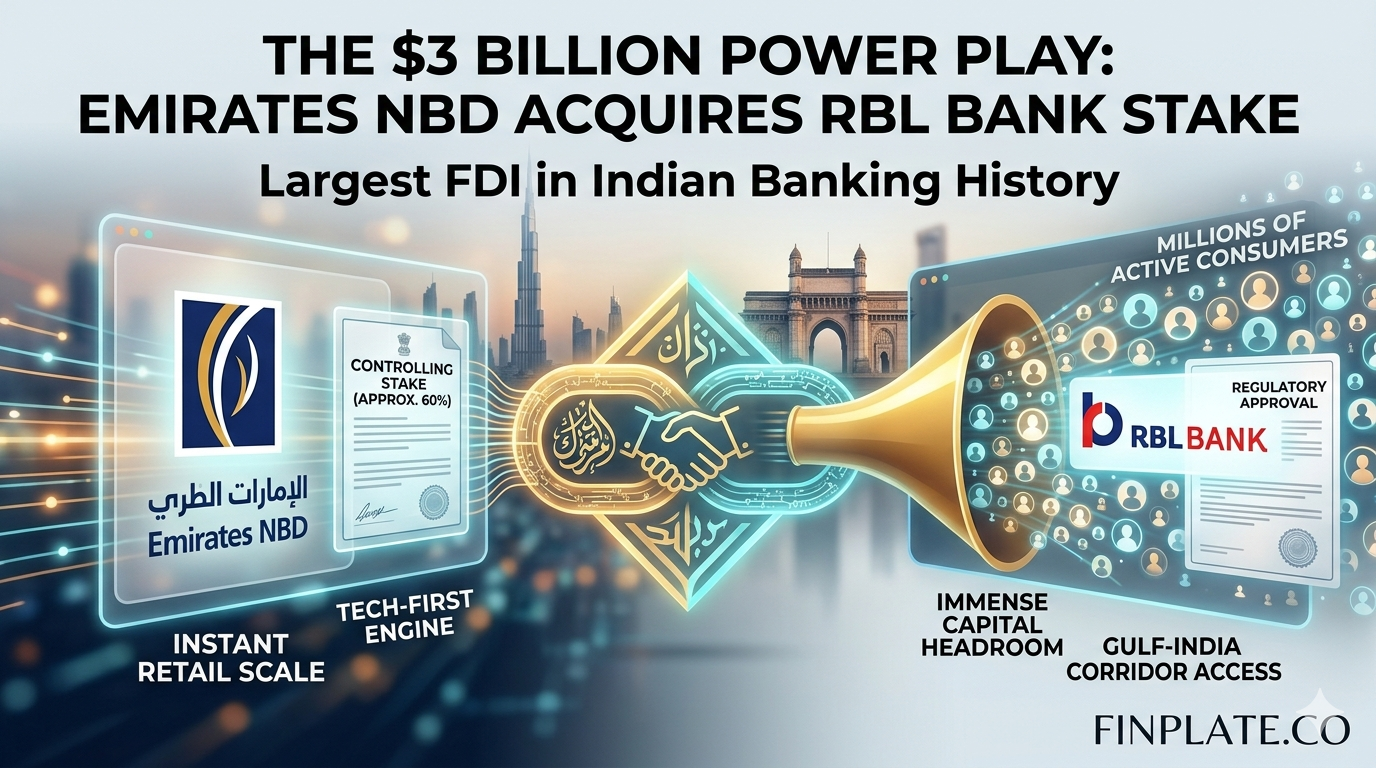

Emirates NBD– The absolute titan of banking in the Middle East has finalized a staggering $3 billion deal to acquire a controlling stake in India’s RBL Bank.

At Finplate.co, we love looking past the massive price tags and corporate press releases to see what’s actually happening behind the curtain. This isn’t just a standard investment or a routine corporate reshuffle. It’s a massive, loud statement about exactly where global money wants to be positioned in 2026.

If you’ve been wondering how international markets view India’s economic engine right now, this deal gives you a definitive answer. Let’s unpack why this massive cross-border move matters to the market, the players involved, and your own financial ecosystem.

1. Why RBL? The Art of the Strategic Shortcut

Think about it this way: if you want a premium house in a prime, highly competitive neighborhood, what do you do? Do you buy an empty plot of land, hire architects, fight for municipal permits, and wait five painful years to build it from scratch? Or do you just buy the best, most modern house already standing on the block?

Emirates NBD chose the shortcut. Building a brand-new banking network in India from the ground up is notoriously difficult. The regulatory paperwork is intense, customer trust takes decades to earn, and setting up physical and digital infrastructure cost billions before you even see a rupee in profit.

By acquiring a controlling stake in RBL Bank, the Dubai-based giant instantly inherits an incredible, pre-built asset:

- A Tech-First Retail Engine: RBL was an early adopter of open banking APIs and modern fintech partnerships, meaning their infrastructure is built for the modern era.

- A Credit Card Powerhouse: RBL has carved out a highly successful, high-margin niche in the credit card and micro-banking segments.

- Instant Scale: Instead of fighting for market share customer by customer, Emirates NBD gains millions of active Indian consumers and business accounts overnight.

2. The Hidden Financial Superhighway: The Gulf-India Corridor

To understand the true scale of this deal, you have to zoom out and look at a map. The economic corridor between the United Arab Emirates (UAE) and India is one of the busiest, most lucrative financial channels in the entire world. It is driven by billions of dollars in bilateral trade, massive corporate investments, and constant cross-border payments.

Up until now, moving money seamlessly between these two regions often meant dealing with multiple intermediary banks, high fees, and frustrating delays.

This acquisition completely changes the game:

- For Corporate Businesses: Companies operating across Dubai and Mumbai now have one single, unified banking partner to handle their cash management, trade finance, and cross-border logistics.

- For the NRI Community: It opens up seamless, friction-free wealth management and investment channels for Non-Resident Indians living and working in the Gulf who want to send money back home safely.

By locking down this majority stake, Emirates NBD is essentially building the ultimate, exclusive toll booth on the financial superhighway connecting India and the Middle East.

3. The “Fuel Tank” Effect: Unlocking Massive Growth

Let’s talk about the technical side of banking for a second, but keep it entirely human. Why does a stable, mid-sized Indian bank need a $3 billion global partner in the first place?

It all comes down to leverage and growth capacity. In the banking world, you can’t just give out endless loans out of thin air. To hand out credit safely, banks need a massive cushion of core capital sitting in their reserves.

Right now, India’s hunger for credit is growing faster than almost anywhere else on earth. Everyday citizens want home loans, car loans, and credit cards, while ambitious startups and enterprises need massive capital to scale up.

This $3 billion cash infusion fills RBL Bank’s fuel tank to the absolute brim. It gives them the immense “capital headroom” they need to aggressively expand their digital loan portfolios, open new branches, and absorb any unexpected market bumps without breaking a sweat. It takes them from a strong mid-sized player and hands them the resources to play in the big leagues.

Finplate’s Conceptual Take: The Coming Consolidation Wave

If you’ve been following our educational pieces here on Finplate.co, you know we talk a lot about market cycles. We are officially moving out of the era where the market was fragmented into hundreds of tiny, hyper-specialized financial startups.

2026 is becoming the year of institutional consolidation. When a sovereign-backed global giant like Emirates NBD deploys this much capital across borders, it sets a brand new benchmark. It tells the global financial community that the Indian banking sector isn’t just stable—it’s a premium growth asset.

Don’t be surprised if this move triggers a domino effect, leading other international institutions from Europe, Asia, and Wall Street to start shopping for strategic stakes in mid-sized Indian private banks before the year ends.

The Bottom Line

At the end of the day, this $3 billion power play is proof that global institutional money is incredibly confident in India’s long-term consumer story. The lines dividing global finance and local retail banking are blurring faster than ever. For the average consumer or business owner, this means better technology, more robust financial products, and the peace of mind that comes with massive international backing.

What’s your take? Would you feel more comfortable keeping your money with a local bank that has heavy international backing, or do you prefer traditional, homegrown financial giants?

Explore more deep dives into Fintech M&A at Finplate.co